Early Retirement Budgeting: Your First 5 Years Strategy Guide

- The first 5 years of retirement are the most critical for long-term financial security

- Use spending bands (Floor/Target/Ceiling) instead of fixed budgets

- Start conservative at 3-3.5% withdrawal rate for early retirement

- Maintain 1-2 years of expenses in cash for market volatility

- Every dollar overspent early costs you exponentially more later

Your retirement budget isn't a restriction — it's your roadmap to 30+ years of financial confidence.

Picture this: You've just left your job for the last time. Your portfolio has seven figures. You've read all the retirement books. You're ready to live the dream.

Then reality hits.

The first withdrawal from your retirement account feels strange. The second feels worse. By month six, you're lying awake wondering if you're spending too much, too little, or if you're doing everything wrong.

Welcome to the most fragile phase of your entire retirement budgeting journey.

Why Early Retirement Spending Matters More Than You Think

Here's what nobody tells you about retirement: The first five years determine everything.

It's not just about having enough money — it's about spending it correctly when the stakes are highest. Make mistakes during this critical period, and you could permanently damage your long-term financial security. Get it right, and you set yourself up for decades of confident spending.

The problem? Most retirement advice focuses on accumulation, not decumulation. We discuss the 4% rule endlessly but barely mention what happens when markets crash in year two of your retirement.

What is Sequence of Returns Risk?

The nightmare scenario where poor market performance in your early retirement years destroys your portfolio before it can recover. Unlike during your working years, when you could wait out downturns, you're now withdrawing money every month, turning paper losses into permanent reductions in your nest egg.

The "Go-Go Years" Spending Trap in Early Retirement

Financial planners call early retirement the "go-go years" — when you're healthy, energetic, and finally free to pursue everything you've dreamed about. Travel the world! Take up expensive hobbies! Live it up!

It's also the fastest way to destroy your retirement security.

The trap is seductive. You've saved for decades, denying yourself things you wanted. Now you have a substantial portfolio and unlimited time. Why not front-load the enjoyable expenses?

Because mathematics doesn't care about your bucket list.

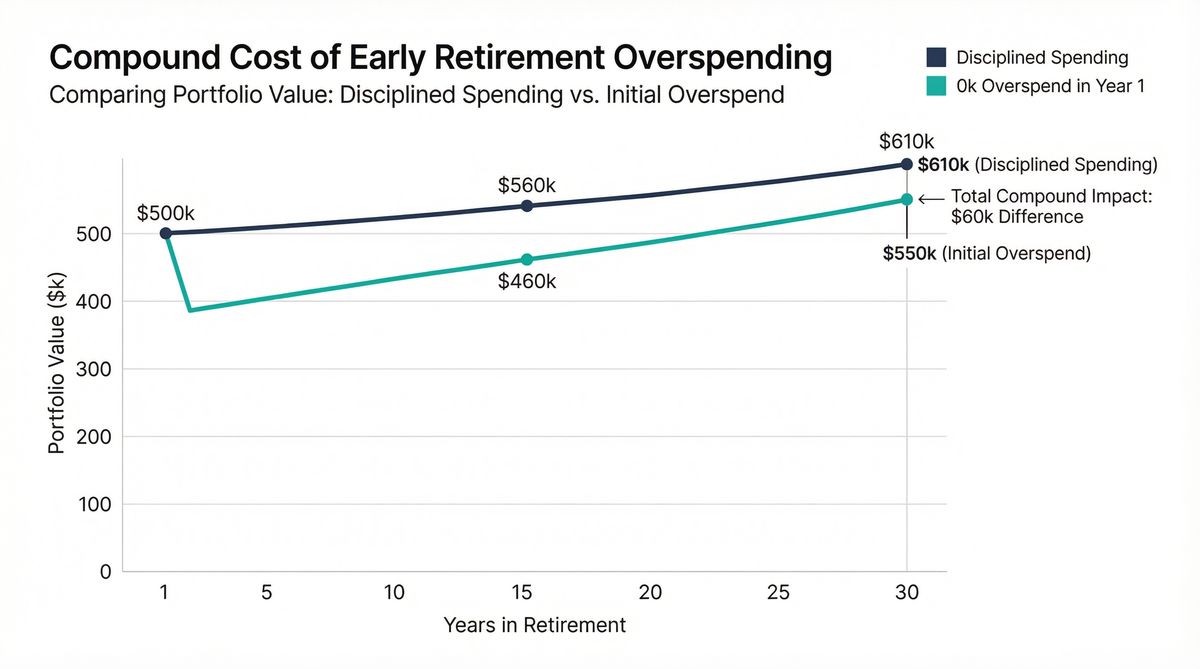

Every dollar you overspend in year one is money that can't compound for the next 30 years. Spend an extra $20,000 on that European river cruise, and you've actually cost yourself approximately $160,000 in today's purchasing power by age 85 (assuming a 7% annual return).

I'm not advocating against travel or enjoyment — I'm advocating for intentionality.

The goal isn't spending less; it's spending smarter when it matters most.

Build a Flexible Retirement Budget (Not a Fixed One)

Forget traditional budgeting approaches. Retirement budgeting isn't about fixed categories and rigid limits. It's about creating guardrails that protect you while allowing you to enjoy your money.

Here's how successful early retirees approach spending:

Start Conservative with Your Safe Withdrawal Strategy

Don't begin retirement by maximizing the 4% rule. If you're retiring before age 65, consider starting at 3% to 3.5%. This provides a buffer for market volatility and healthcare costs before Medicare eligibility begins.

Rosa, a friend who retired at 58 with a $1.2 million portfolio, started by withdrawing just $36,000 in her first year — exactly 3%. She maintained low expenses, watched her portfolio grow, and gradually increased her spending as she gained confidence.

Use Spending Bands in Your Early Retirement Budget

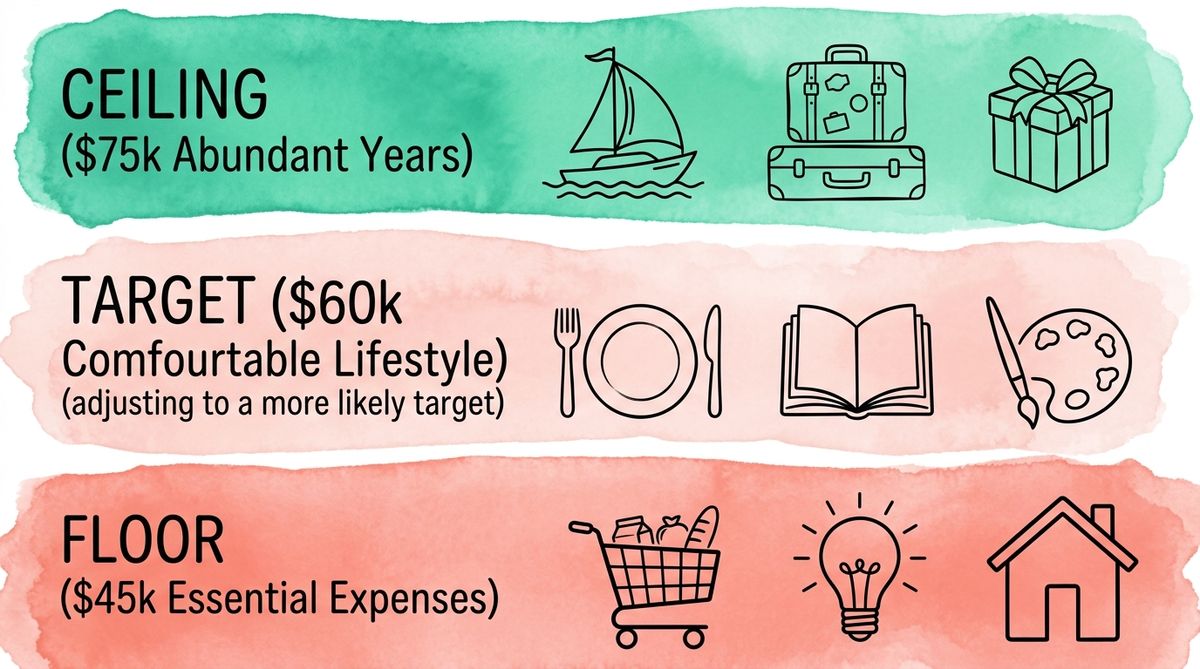

Instead of budgeting exactly $60,000 annually, create three spending levels:

- Floor: $45,000 (essential expenses only)

- Target: $60,000 (comfortable lifestyle)

- Ceiling: $75,000 (abundant years when markets perform well)

This approach allows portfolio-based adjustments without feeling like you're failing at retirement.

Implement the Bucket Strategy for Safe Withdrawals

The bucket approach isn't just investment theory — it's psychological peace of mind. Maintain 1-2 years of expenses in cash or short-term bonds. This allows you to weather market crashes without selling stock investments when they're depressed.

David in Portland maintains exactly 18 months of expenses in a high-yield savings account. "It's not the most efficient approach," he explains, "but I sleep soundly knowing I don't need to sell stocks during bear markets."

Retirement Budgeting Guardrails: When to Adjust Your Strategy

The difference between retirees who deplete their funds and those who don't isn't luck — it's having clear rules for spending adjustments in their safe withdrawal strategy.

Portfolio Gained 5%+

- Consider modest spending increase

- Maybe upgrade from Floor to Target

- Book that delayed vacation

- Stay disciplined — don't get greedy

Portfolio Down 10%+

- Reduce discretionary expenses

- Move from Target to Floor spending

- Delay major purchases

- Remember — this is temporary

The Annual Portfolio Performance Check

Each January, evaluate your portfolio's previous year performance. This isn't about perfect optimization — it's about systematic responses to market realities without panic or paralysis.

Healthcare Costs in Early Retirement Budgeting

Healthcare expenses can be devastating for early retirees. Without employer insurance, family coverage might cost $1,500+ monthly. Include this in your essential spending floor, not discretionary budget.

The Major Purchase Test for Early Retirement Spending

Before significant expenses — new vehicles, home renovations, extended travel — ask yourself: "Would I be comfortable with this expenditure if my portfolio declined 25% next month?" If not, delay or reduce the expense.

Warning Signs vs. Normal Retirement Budget Anxiety

Normal retirement concerns: "Did I withdraw too much this month?"

Genuine red flag: Your portfolio declined 15% and you're maintaining full planned withdrawals.

Normal market behavior: Account values fluctuate with markets.

Time to adjust: You've been selling invested assets for 12+ consecutive months.

The objective isn't eliminating all risk or worry — it's distinguishing between normal retirement adjustments and genuine warning signals requiring action.

The 80% Rule

Start your retirement with 80% of your planned spending to build confidence. You can always increase later, but you can't undo the damage from early overspending.

Your First-Year Retirement Budgeting Strategy

Smart early retirees follow this approach in their initial 12 months:

Your First-Year Action Plan

- Begin with 80% of planned spending to build confidence and create a safety buffer

- Track all expenses for six months to understand your actual cost patterns

- Schedule quarterly portfolio reviews to identify problems before they become crises

- Limit major purchases until you've experienced a full market cycle as a retiree

- Establish cash reserves first before optimizing investment allocations

Remember: You can always increase spending later. You cannot undo damage from overspending during bear markets.

The Bottom Line on Early Retirement Budgeting

Early retirement spending isn't about spending less — it's about spending intelligently when stakes are highest. These first five years will teach you more about money management than decades of wealth accumulation.

Successful long-term retirees aren't those with the largest portfolios. They're those who master flexibility without recklessness, generosity toward themselves without foolishness.

Your retirement budgeting strategy isn't a restriction — it's your roadmap to 30+ years of financial confidence.

The goal isn't dying with the most money. It's living well without running out.