SECURE 2.0 Act 2026: New Catch-Up Limits Save You $13K

Published March 19, 2026 • 8 min read

So back in December 2022, Congress passed this thing called the SECURE 2.0 Act. Made headlines for about five minutes. Then everyone went back to arguing about TikTok and whether pineapple belongs on pizza.

The big SECURE 2.0 changes hit in 2026, especially if you're 60-63:

- Super catch-up contributions: Ages 60-63 can put away $35,750 total (vs. $32,500 for everyone else)

- Mandatory Roth rule: High earners ($145k+) must make catch-ups Roth-only

- Emergency savings accounts: Up to $2,500 built into your 401(k)

- Higher limits across the board: 401(k) base up to $24,500, IRA catch-ups finally inflation-adjusted

Action: If you're 60-63, this could save you $13,000+ in extra tax-advantaged space over four years.

But here's the thing nobody's talking about — most of the good stuff doesn't kick in until 2026. And I mean really good stuff, especially if you're in that sweet spot between 60 and 63 where you're probably earning peak money but also quietly freaking out about whether you've saved enough.

We're talking about a brand-new "super catch-up" that lets you stuff an extra $11,250 into your 401(k) on top of everything else. A weird mandatory Roth rule that's gonna blindside a bunch of people who make decent money. And some other SECURE Act changes that could actually matter if you know about them.

Maybe your HR department hasn't mentioned any of this. Your 401(k) company will send you a boring letter in October when it's too late to do anything useful. So let's break it down now while you can actually act on it.

Super Catch-Up Contributions 2026: Four Years to Go Nuts

If you're between 60 and 63 in 2026, you just won the lottery. Kind of.

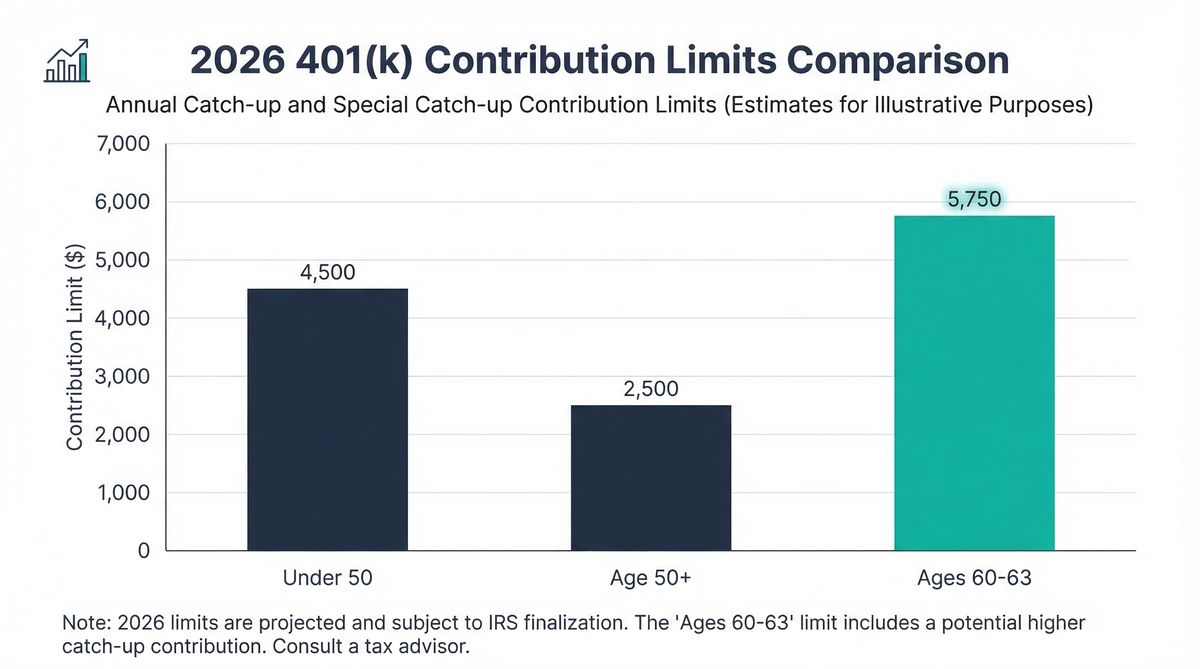

Quick background: If you're 50 or older, you've always been able to make "catch-up contributions" to your 401(k). In 2026, that's $8,000 on top of the regular $24,500 limit. Not terrible.

But the SECURE 2.0 Act created this new thing for people aged 60-63: the super catch-up contributions. Instead of $8,000 extra, you get $11,250 extra.

That's $35,750 you can put away in a single year. Total.

The $13K Advantage

If you max out these retirement catch up limits 2026 from age 60 to 63, you're looking at $13,000 more in catch-up contributions compared to the regular limits. All tax-advantaged.

My friend David turned 60 last month and when I told him about this, he literally called his payroll person the next day. Smart man.

This isn't just 401(k)s either — 403(b)s, government 457 plans, even the TSP if you're a fed.

Why These New Contribution Limits Actually Matter

Ages 60-63 are often when people finally have some breathing room. Kids are gone. Mortgage might be done. You're probably making the most money you'll ever make.

But here's the kicker: it's only four years. Turn 64? Back to regular catch-up limits. Miss a year? That money's gone forever. You can't make it up later.

I've got another friend, Rosa, who's 62. She's got two years left in this window. Two years to basically turbo-charge her retirement. She's treating it like the gift it is.

SECURE 2.0 Roth Rules That'll Mess People Up

This one's sneaky as hell, and honestly, most people have no idea it's coming.

If you made more than $145,000 in 2025, all your 2026 catch-up contributions have to be Roth. Period. No choice.

Important Detail

This rule is based on what you made last year. So your 2025 paycheck determines what happens with your 2026 savings. It's based on FICA wages from your W-2, not total income.

For years, high earners have been doing pre-tax catch-ups to lower their taxes. That party's over if you're above the threshold.

The Part That Really Sucks About These SECURE Act Changes

If your company doesn't offer Roth 401(k) options — and plenty still don't — you might not be able to make catch-up contributions at all.

Like, zero. Nothing.

My client Steve works for a mid-sized company that's still stuck in 2005. No Roth option. He made $180k last year. Come 2026, he's locked out of catch-up contributions entirely unless they get their s*** together.

If this sounds like you, go bug your HR people. Now. Not next month. This isn't something they can flip a switch on.

But These New Retirement Rules Aren't All Bad

Yeah, you lose the upfront tax break. For someone in the 32% bracket, that's about $2,560 more in taxes on $8,000 of catch-up money.

But you get something better: tax-free forever. No taxes on the growth. No taxes when you pull it out. If you're not touching this money for 10+ years, the math usually works out in your favor.

Plus, let's be real — tax rates probably aren't going down. The government's gonna need revenue from somewhere.

2026 Retirement Contribution Limits: All the Numbers You Need

Since we're talking numbers, here's everything you need to know for retirement planning in 2026:

401(k) and Similar Plans

| Contribution Type | 2026 Limit | Who Qualifies |

|---|---|---|

| Regular limit | $24,500 | Everyone |

| Normal catch-up | $8,000 | Age 50+ |

| Super catch-up | $11,250 | Ages 60-63 only |

| Max if you're 60-63 | $35,750 | The sweet spot |

| Max everyone else | $32,500 | Ages 50-59 or 64+ |

IRA Contribution Limits 2026

| Account Type | 2026 Limit | Notes |

|---|---|---|

| Regular IRA limit | $7,500 | Up from $7,000 |

| Catch-up (50+) | $1,100 | First increase since 2006! |

| Max total | $8,600 | Finally inflation-adjusted |

Fun fact: IRA catch-ups were stuck at $1,000 for twenty years. The SECURE 2.0 Act finally made them inflation-adjusted. About time.

HSA Limits (Not SECURE 2.0 But Still Important for Retirement)

HSAs are still the best retirement account nobody talks about. Triple tax advantage. If you've got a high-deductible plan, max this thing out.

- Solo coverage: $4,400

- Family: $8,750

- Catch-up (55+): $1,000

Emergency Savings Accounts: Finally, Something Practical

Here's a SECURE Act provision that actually makes sense for normal humans: emergency savings accounts built right into your 401(k).

Your employer can now offer you a side account with up to $2,500 that you can hit up for emergencies without wrecking your retirement savings. You can take money out at least once a month, no penalties, no taxes, no paperwork nightmare.

Real-World Impact

Kim's company rolled this out last year. She's been putting $100 a month into it. Last month, her washing machine died and instead of taking a 401(k) loan, she just pulled $800 from the emergency account. Bam.

It's not life-changing money. But for people who've been choosing between building an emergency fund and saving for retirement, it's brilliant. You can do both.

Real People Using SECURE 2.0 Changes: The Numbers

Let me show you what these new retirement savings rules look like for actual humans.

The Power Couple Maximizing Super Catch-Up

Mark & Linda (Both 62)

- Each can contribute $35,750

- Combined 401(k) savings $71,500

- Add their IRAs +$17,200

- Total tax-advantaged $88,700/year

Two-Year Window Impact

- Years 62-63 combined $177k+

- vs. regular catch-up $26k less

- Peak earning years Maximized

- Retirement acceleration Massive

The High Earner Facing SECURE 2.0 Roth Requirements

Sarah makes $200k and just found out her catch-ups have to be Roth. She's pissed about losing the tax deduction.

I told her to think about it differently. She's 55. That money's not getting touched for at least 10 years. If it doubles (totally reasonable), she's avoiding taxes on the entire gain. The forced Roth thing might actually be doing her a favor.

But first, she needs to make sure her employer offers Roth 401(k). If they don't, she's screwed.

The Emergency Fund Guy Using New SECURE Act Features

James makes $55k and has been stressed about not having an emergency fund because every dollar goes toward getting his 401(k) match.

His company started offering the emergency savings account. Now he's building to $2,500 while still getting his match. When his car needed work, he didn't have to raid his retirement. Problem solved.

What You Should Do About SECURE 2.0 Act 2026 Changes

Don't sit on this information. Here's your retirement planning to-do list:

🎯 Your SECURE 2.0 Action Plan

- If You're 60-63: Figure out if you can max the super catch-up ($35,750 total). Adjust your payroll now — don't wait until July and then try to cram $20k into six months of paychecks.

- If You Made Over $145k Last Year: Check if your company offers Roth 401(k). If they don't, start making noise. This isn't optional anymore — you'll be locked out of catch-ups without it.

- Everyone Else: Bump up your savings if you can. The 2026 contribution limits went up across the board. Ask about emergency savings accounts. Don't forget your IRA — the catch-up finally increased.

The Bottom Line on SECURE 2.0 Act Benefits

The SECURE 2.0 Act is probably the biggest retirement law change in decades, but because it's rolling out in pieces over several years, nobody's paying attention.

That's your opportunity. While everyone else is sleeping, you can take advantage. The super catch-up alone could mean an extra $13k in tax-advantaged space over four years. The Roth rules, handled right, could save you serious money down the road.

At Ready Aim Retire, we're building tools to show you exactly how these SECURE Act changes affect your situation. Because knowing you can contribute $35,750 doesn't help if you can't figure out what that means for your actual retirement timeline.

Check out our retirement calculator to model how these new limits affect your retirement date. And if you want to understand how emergency savings accounts work with your overall strategy, our emergency fund guide breaks it down step by step.

2026's here. The sooner you move, the more you win.

Cheers!