SECURE 2.0 Emergency Savings: Your 401k Emergency Fund Starts in 2026

Here's something that keeps me up at night: watching smart people make dumb money decisions because the system's broken.

My friend Marcus called me last month, stressed out of his mind. His car needed $1,800 in repairs, and he was about to cash out part of his 401(k) to cover it. "I know it's stupid," he said, "but I don't have anywhere else to get the money."

This is the trap millions of people fall into. The financial advice industry tells you to build a massive emergency fund before even thinking about retirement. But if you're making $60k and trying to save $20k for emergencies, that's literally 33% of your gross income sitting in a savings account earning nothing while your future self gets screwed.

It's a rigged game. And frankly, I'm tired of pretending it makes sense.

But here's the good news: Starting in 2026, Congress actually did something useful. The SECURE 2.0 Act lets your employer add a 401k emergency fund directly to your retirement plan that you can tap penalty-free. Up to $2,500, no questions asked, no bureaucratic BS.

It's not perfect, but it's progress. And for people like Marcus, it could be a game-changer.

If you don't have time to read the full breakdown, here are the main points:

- Starting 2026: Your employer can add a $2,500 emergency savings account to your 401(k)

- No penalties: Withdrawals are penalty-free and tax-free (after-tax contributions)

- Income limit: Only available to employees making under $150,000

- Game changer: Removes the choice between emergency savings and retirement

This isn't about replacing all emergency planning-it's about handling the small emergencies that currently derail people's financial progress.

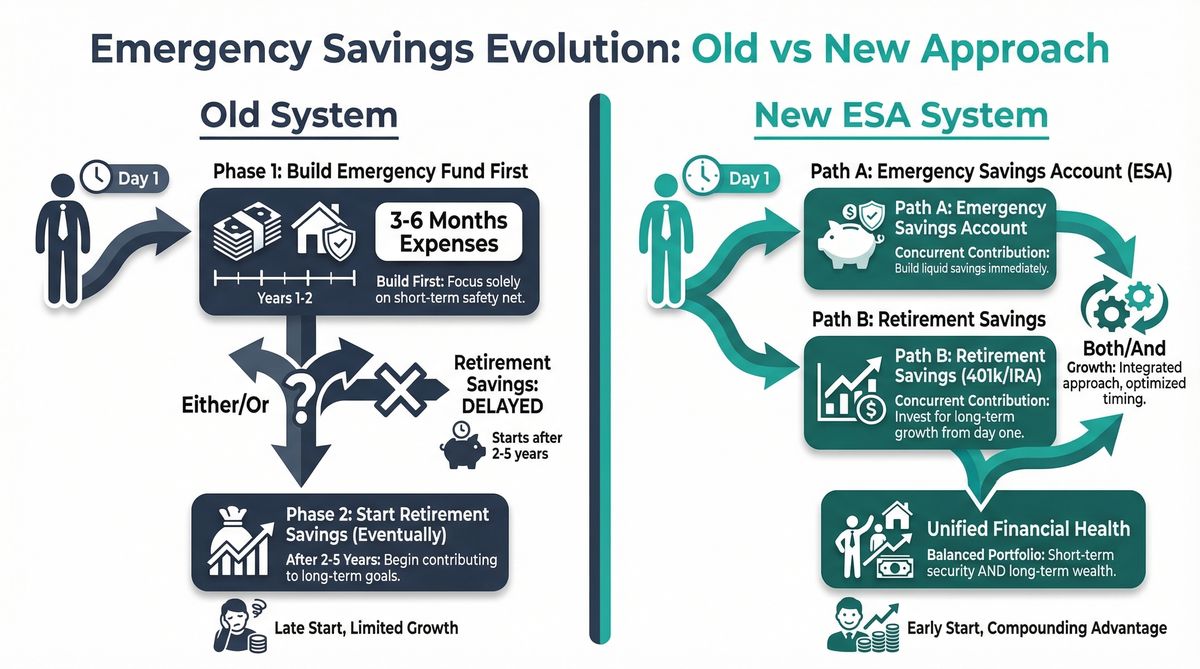

The Problem: When Emergency Funds Compete With Retirement Savings

Let me paint you a picture of how absurd our current system is.

Traditional financial wisdom says you need three to six months of expenses saved before you contribute to retirement beyond your employer match. So if you spend $4,000 a month, you need $12,000-$24,000 just sitting there earning 1% interest before you can start building wealth.

That's insane.

While you're dutifully saving for hypothetical emergencies, you're missing out on:

- Employer matching (free money you'll never get back)

- Compound growth (the most powerful force in finance)

- Tax advantages (because apparently the IRS occasionally does nice things)

And here's the kicker: When real emergencies hit, people don't use their carefully curated emergency funds. They panic and raid their 401(k) anyway.

The Fed says 40% of Americans can't cover a $400 emergency. Meanwhile, the average hardship withdrawal is $5,000-$10,000, getting hit with a 10% penalty and leaving permanent damage to retirement security.

It's like telling someone not to use the fire extinguisher because they might need it later, then watching them burn their house down.

SECURE 2.0 Emergency Savings Account: How It Actually Works

Here's what the SECURE 2.0 emergency savings account actually does—without the financial industry jargon.

What is a SECURE 2.0 Emergency Savings Account?

Emergency Savings Account (ESA): A separate account within your 401(k) plan specifically for emergency savings. You contribute after-tax money through payroll deduction, can withdraw penalty-free up to $2,500, and it's only available to employees earning under $150,000 annually.

Who gets it: Anyone making under $150k (sorry, tech bros, this one's not for you).

How it works: Your employer can add a separate emergency bucket to your 401(k). You contribute after-tax money through payroll deduction, and penalty-free 401k withdrawals come out tax-free because you already paid the IRS.

The limit: $2,500 max. Once you hit that, new contributions automatically go to your regular 401(k).

Getting your money: Works like a debit card or bank transfer. No paperwork, no proving your emergency is "emergency enough," no penalties.

The catch: Your employer can set some reasonable limits, like once-a-month withdrawals or minimum amounts. But nothing like the bureaucratic nightmare of hardship withdrawals.

This eliminates the biggest psychological barrier to emergency funds: the fear that your money's locked away when you need it most.

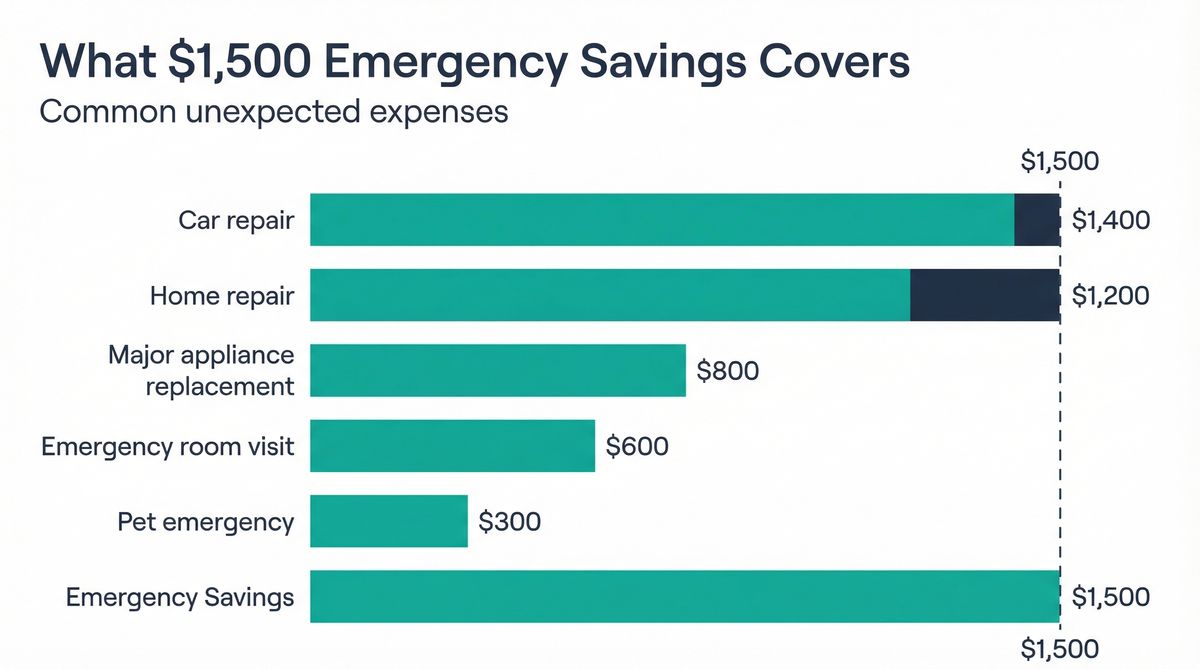

Why $2,500 Emergency Savings Account 2026 Limits Make Sense

Before you roll your eyes about the "small" limit, let me tell you what $2,500 covers:

My neighbor Jenny hit a deer last winter. Repair bill: $1,400.

My buddy Carlos had a kidney stone that sent him to the ER. After insurance: $900.

When my washing machine died last year (because of course it did), replacement cost: $600.

Key Insight: Small Emergencies, Big Impact

Most financial emergencies aren't the catastrophic job-loss scenarios we obsess over. They're the annoying, expensive surprises that derail your budget if you're not prepared.

For bigger emergencies—like when my friend Rosa's roof started leaking—$2,500 buys you time to figure out the rest. Instead of panicking and cashing out $8,000 from your 401(k), you use your emergency account to handle immediate needs while you arrange financing for the big stuff.

Here's where it gets interesting: Some employers might offer 401(k) matching based on your emergency savings contributions. That's free money on money you're saving for emergencies. Show me a bank account that does that.

Penalty-Free 401k Withdrawal Strategy (Without the Corporate Speak)

Look, I'm not gonna sugarcoat this—having easy access to your money is both awesome and dangerous. Here's how to not screw it up:

- Contribute smart: Get your full employer match first. That's still priority #1. Then build your emergency account. Then pump up retirement contributions.

- Define "emergency": Write down what counts as an emergency before you're in crisis mode. Car repairs? Yes. New iPhone? No. Be honest with yourself.

- Ask the right questions: Find out if your employer's ESA contributions trigger 401(k) matching. If yes, this becomes a no-brainer.

- Plan for the future: If you're climbing the income ladder and might hit $150k, max out your ESA contributions now while you still can.

Here's my take: This isn't meant to replace all emergency planning. It's meant to handle the small-to-medium emergencies that currently force people to make terrible financial decisions.

401k Emergency Fund: Common Questions Answered

"Should I ditch my regular savings account?"

Nah, don't go crazy. Keep some money outside your workplace plan. The $2,500 limit means you'll need more for big emergencies anyway. Plus, some of us like having money that's completely disconnected from work drama.

"What happens to my 401k emergency fund if I change jobs?"

Unlike those predatory 401(k) loans (seriously, f*ck those things), your emergency account doesn't need immediate repayment when you leave. The rules are still being worked out, but it stays accessible during job transitions—exactly when you might need it.

"Isn't this just encouraging people to save less for retirement?"

Only if you're an idiot about it. Used right, this helps people save MORE for retirement by removing the excuse that they need to choose between emergency and retirement savings.

"How's this different from a Roth IRA?"

Roth IRA contributions come out penalty-free anytime, but good luck setting up automatic payroll deduction to one. ESAs make saving automatic and effortless, which matters more than most people realize.

SECURE 2.0 Emergency Savings: The Bigger Picture

This isn't just about emergency accounts. It's about acknowledging that human psychology matters more than perfect financial theory.

For decades, we've been telling people to be perfectly disciplined savers who can delay gratification indefinitely. But humans don't work that way. We're wired to prioritize immediate threats over future benefits.

The ESA says, "Fine, you want security? Here's security. Now will you please start saving for retirement?"

Old System

- Emergency Priority First

- Timeline to Start Retirement 2-5 years

- Choice Required Either/Or

- Result Delayed retirement saving

New ESA System

- Emergency Priority Simultaneous

- Timeline to Start Retirement Immediate

- Choice Required Both/And

- Result Accelerated wealth building

It's like automatic enrollment for 401(k)s, which boosted participation rates by removing the need to make active decisions. Sometimes the best policy is the one that works with human nature instead of against it.

When people feel financially secure, they make better long-term choices. They don't cash out their 401(k) when changing jobs. They increase contributions when they get raises. They take appropriate investment risks instead of hiding everything in conservative funds.

This stuff matters beyond individual bank accounts.

Emergency Savings Account 2026 Implementation Timeline

The ESA feature launches in 2026, but don't expect every employer to jump on it immediately.

Big companies with solid HR teams will probably adopt it quickly. They love benefit features that sound innovative and don't cost them money.

Smaller employers will take longer because it requires plan provider upgrades and more administrative work. If your company doesn't offer it right away, bug your HR person about when they're planning to add it.

The big retirement companies—Fidelity, Vanguard, the usual suspects—are building the tech infrastructure now. Success will depend on making withdrawals as easy as they promise, not some clunky system that requires three phone calls and a blood sample.

Bottom Line: SECURE 2.0 Emergency Savings Changes the Game

Look, the SECURE 2.0 emergency savings account isn't going to solve poverty or fix our broken healthcare system. But it does address one specific, stupid problem: the false choice between emergency security and retirement preparation.

For anyone making under $150k (which is most of us), it offers a path to financial stability that doesn't require choosing between today and tomorrow.

The key is treating it like what it is: one tool in a broader financial toolkit. Max your employer match, build your emergency account, then focus on retirement contributions and other savings goals.

As these features roll out, tools like Ready Aim Retire's retirement calculator will help you figure out how emergency savings accounts fit into your specific situation. Because personal finance is personal, and what works for my friend Marcus might not work for you.

But at least now you'll have more options than "save everything or save nothing."

The system's still far from perfect, but sometimes small wins add up to something bigger. This is one of those times.

🎯 Your Next Steps for 2026

- Ask HR: Find out if your employer plans to add ESA features and when

- Plan your strategy: Decide how ESAs fit into your current emergency fund approach

- Maximize employer match: Still priority #1, then consider ESA contributions

- Set clear rules: Define what counts as an "emergency" before you need the money

Thanks for reading if you've made it this far. Now go check if your employer's planning to add this feature, and start thinking about how $2,500 in accessible emergency cash might change your financial picture.

Peace!