How to Increase Your Retirement Income: 9 Strategies That Actually Move the Needle

By Ross Williams • Published May 23, 2026

I was sitting with my friend Tom last year, going over his retirement numbers on the back of a napkin at a coffee shop in Denver. He and his wife Sarah had about $800,000 saved up, a $2,000 monthly Social Security check, and a small pension. Not bad at all. But as we started running different scenarios, I watched his eyes get wide. Depending on just a handful of decisions, their annual retirement income could swing by $15,000 to $25,000. Without saving another dime.

Nine strategies to boost retirement income by $10,000-$25,000 annually:

- Delay Social Security to age 70 for 77% more benefits

- Use Roth conversions during the "retirement income valley"

- Implement tax-efficient withdrawal sequencing

- Claim the new $6,000 senior tax deduction

- Leverage Qualified Charitable Distributions to reduce taxes

- Lock in today's 5-6% annuity rates

- Consider strategic part-time work

- Max out HSA before Medicare eligibility

- Downsize strategically to unlock home equity

The key is coordination: these strategies work together to create significantly higher lifetime income.

That gap comes down to timing, tax planning, and knowing which levers to pull. Most retirees leave real money on the table because strategies to increase retirement income are scattered across dozens of articles and nobody puts it all in one place. So let's do that right now, with real numbers.

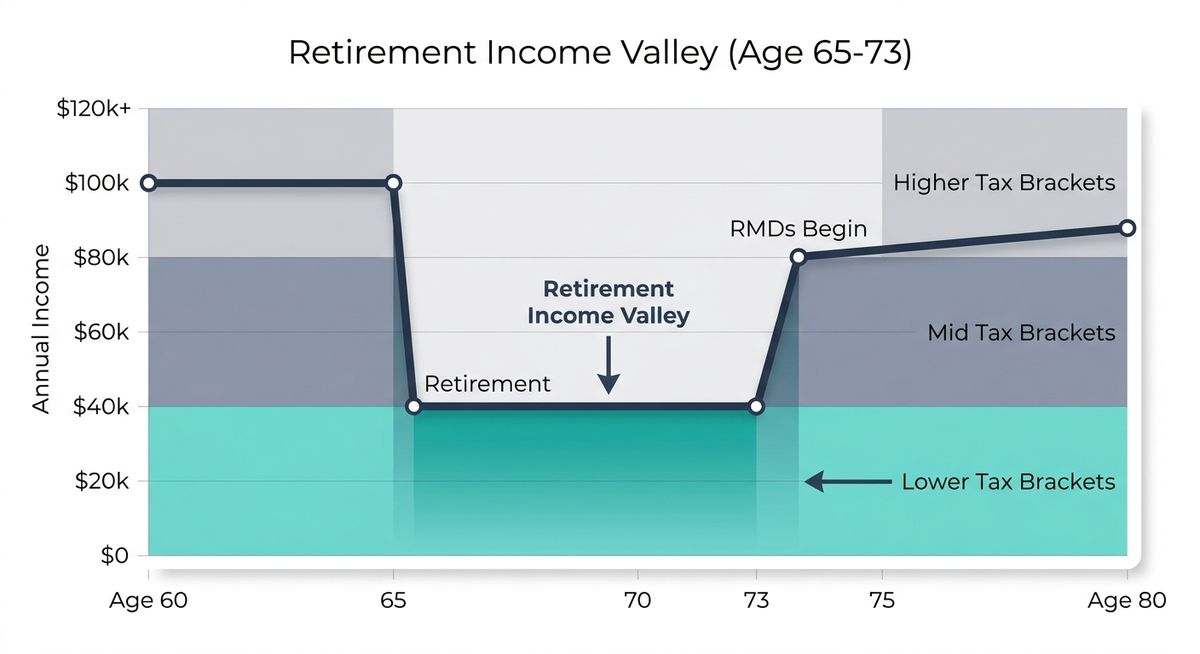

The "Retirement Income Valley" (and Why It's Your Best Opportunity)

The Retirement Income Valley

Between retirement and age 73-75 (when RMDs begin), your taxable income naturally drops. This creates the best window to restructure your finances for higher lifetime income.

Between the day you retire and the day Required Minimum Distributions kick in (age 73 for most people, 75 if you were born in 1960 or later), something interesting happens. Your taxable income drops. You're not earning a salary anymore, and you're not yet forced to pull money from tax-deferred accounts.

Financial planners call this the "retirement income valley." It's the single best window to restructure your finances for higher lifetime income. And most people just cruise right through it without a second thought.

Everything below connects back to this valley. If you remember one thing from this whole article, make it this.

1. Delay Social Security for Maximum Income Growth (Up to 77% More)

This is the most powerful income lever most retirees have. And it doesn't cost you a thing.

Let me show you what the numbers actually look like. Say your Full Retirement Age benefit is $2,000 per month:

Early Claiming (Age 62)

- Monthly Benefit $1,400

- Annual Income $16,800

- 20-Year Total $336,000

Delayed Claiming (Age 70)

- Monthly Benefit $2,480

- Annual Income $29,760

- 20-Year Total $595,200

That's $12,960 more per year by waiting until 70 versus claiming at 62. Over 20 years of retirement, the cumulative difference exceeds $259,000. That's real money.

The Bridge Strategy

Use savings from taxable accounts or Roth IRAs during the valley years (62 to 70) to cover expenses while your Social Security benefit grows by 8% per year. For married couples, coordinate your claiming ages so the higher earner delays to 70 while the lower earner claims earlier to provide bridge income.

But here's what most articles miss. The gap actually widens every year. Cost-of-living adjustments (2.8% in 2026) are calculated as a percentage of your benefit. A 2.8% COLA on a $2,480 benefit adds $69 per month. That same COLA on a $1,400 benefit? Only $39. The higher base compounds permanently.

Not everyone can wait, and that's totally fine. Health issues, limited savings, or urgent expenses can make early claiming the right call. But if you can afford to delay even a few years past 62, every month of waiting increases your benefit permanently. For a detailed breakdown of optimal claiming strategies, see our guide on when to claim Social Security based on your specific age and situation.

2. Strategic Roth Conversions During the Valley

This is where the retirement income valley really pays off.

A married couple filing jointly with no other income can convert up to roughly $133,000 per year from a traditional IRA to a Roth IRA while staying in the 12% federal tax bracket (a blended effective rate under 9%). That's an incredibly low price to move money into an account that will never be taxed again.

Why Roth Conversions Boost Income

Every dollar you convert to Roth is a dollar that won't inflate your Required Minimum Distributions later. Smaller RMDs mean lower taxes in your 70s and 80s, which means more of your money stays in your pocket.

Back to my friends Tom and Sarah. Both 63, with $800,000 in traditional IRAs. If they convert $60,000 to $80,000 per year for ten years before RMDs begin at 73, they'll pay roughly $5,000 to $8,000 annually in conversion taxes at those lower brackets. But by 73, they've moved $600,000 to $800,000 into Roth accounts. Their future RMDs are dramatically reduced, their tax bills in their 70s and 80s are lower, and the Roth money grows tax-free for the rest of their lives.

That's a trade I'd make every single time. For comprehensive strategies on timing and amounts, check out our detailed guide to Roth conversion strategies and optimization techniques.

The IRMAA Trap to Watch

Medicare Part B and D premiums use a two-year lookback. A large Roth conversion in 2026 could push your 2028 Medicare premiums higher by $1,148 to $6,936 per person per year. The income thresholds are $109,000 for single filers and $218,000 for joint filers. Plan your conversion amounts to stay below these cliffs, or at least factor the temporary premium increase into your math.

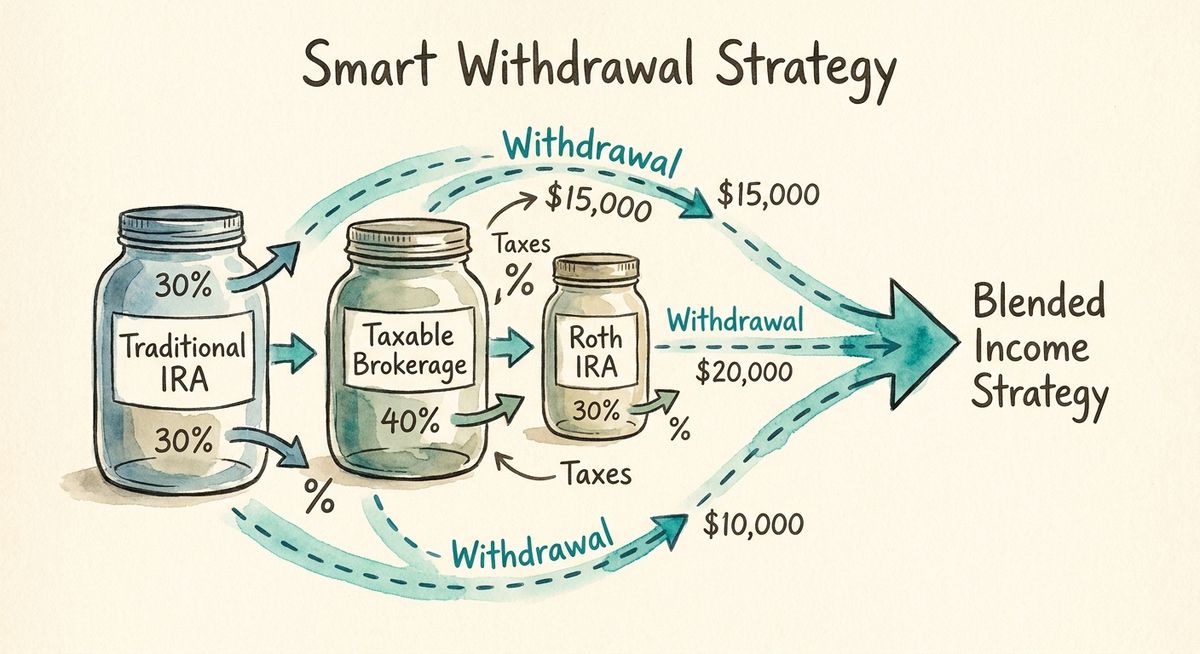

3. Tax-Efficient Withdrawal Sequencing

Most retirees withdraw from whichever account feels convenient. That's an expensive habit.

The conventional wisdom says withdraw from taxable accounts first, then tax-deferred (traditional IRAs, 401(k)s), then Roth accounts last. But the smarter approach is blending withdrawals across account types each year to stay in the lowest possible tax bracket.

Here's what that looks like in real life. Say you need $70,000 in a given year. Instead of pulling it all from your traditional IRA (and paying taxes on every dollar), you might take $30,000 from your traditional IRA, $25,000 from a taxable brokerage account, and $15,000 from your Roth. The traditional IRA withdrawal fills up the lower tax brackets. The brokerage withdrawal might qualify for 0% long-term capital gains rates if your taxable income stays below $98,900 (married filing jointly in 2026). And the Roth withdrawal adds zero to your taxable income.

Same spending. Thousands less in taxes. That tax savings is effectively more retirement income in your pocket.

The 0% Capital Gains Opportunity

In years when your taxable income is low (especially during the valley), you can sell appreciated investments in taxable accounts and pay zero federal capital gains tax. This "harvesting" resets your cost basis higher, reducing future tax liability on those investments. It's one of the nicest freebies in the tax code.

4. Claim the New $6,000 Senior Tax Deduction

The One Big Beautiful Bill Act created a new tax deduction of $6,000 per person age 65 or older ($12,000 for a married couple). This is on top of the standard deduction and the existing additional standard deduction for seniors. It applies to tax years 2025 through 2028.

For a married couple where both spouses are 65 or older, the combined standard deduction, age-related additional deduction, and new senior deduction totals roughly $47,500 in 2026. That means a couple whose only income is Social Security and a modest pension could owe zero federal income tax. Zero.

Important Details

This deduction phases out between $75,000 and $175,000 for single filers and $150,000 to $250,000 for joint filers. It's also temporary, sunsetting after 2028. If you're in the phase-out range, this is another reason to manage your income carefully through withdrawal sequencing and Roth conversion timing.

5. Use Qualified Charitable Distributions to Boost Spendable Income

If you're 70½ or older and donate to charity, Qualified Charitable Distributions are one of the most overlooked income boosters out there.

Here's how it works. Instead of taking your Required Minimum Distribution as income and then donating cash to charity, you direct up to $111,000 ($222,000 for married couples) straight from your IRA to a qualified charity. The donation satisfies your RMD but never shows up as taxable income.

My friend Barbara is 74. She has a $500,000 IRA and a roughly $19,600 RMD. She normally donates $10,000 per year to her church. By routing that $10,000 through a QCD instead of writing a personal check, she reduces her taxable income by $10,000. In the 22% bracket, that saves her $2,200 in federal taxes, and it might keep her below an IRMAA threshold.

She's giving the same amount to the same charity. She just gets to keep $2,200 more of her own money.

I love this strategy because it literally changes nothing about your generosity. You just get to keep more. Many retirees miss this opportunity entirely—learn about other common RMD mistakes that cost retirees thousands.

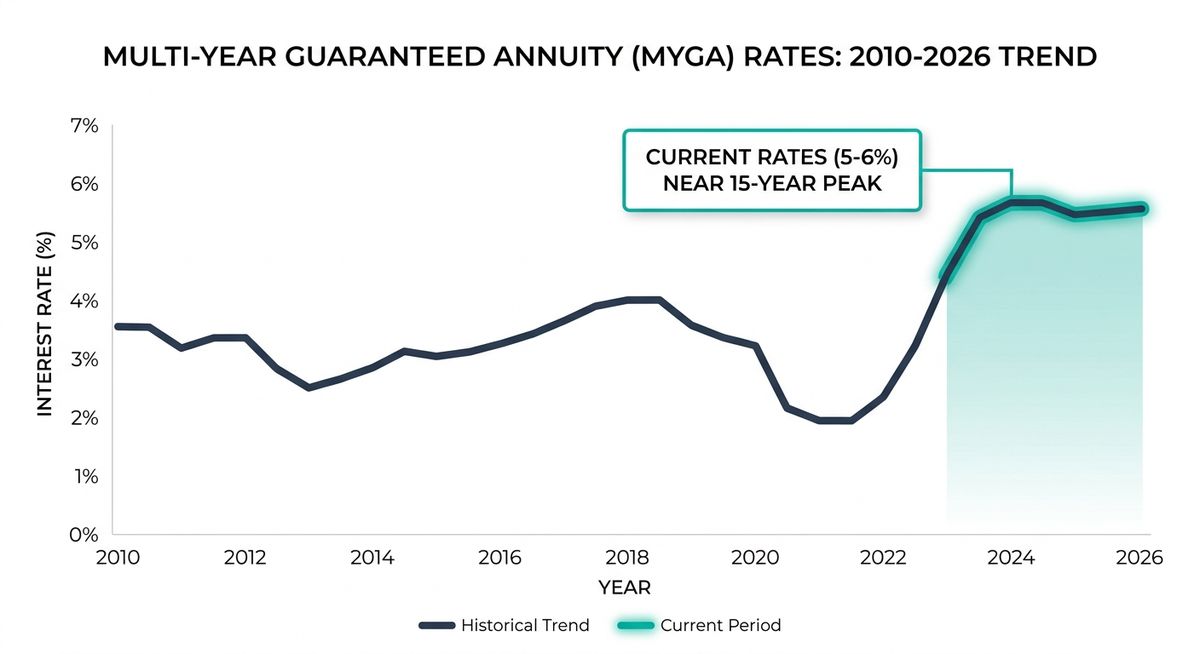

6. Lock in Today's Annuity Rates

Multi-Year Guaranteed Annuities (MYGAs) are paying 5.0% to 6.5% right now, near 15-year highs. These work like CDs but are issued by insurance companies, and they can provide a predictable income floor that takes the anxiety out of market ups and downs.

J.P. Morgan's research found that households with more guaranteed income sources tend to spend up to 44% more in retirement. The psychological effect is real. When you know your baseline expenses are covered by predictable income (Social Security, pensions, annuities), you're more willing to actually spend from your portfolio. And isn't that kind of the whole point?

A MYGA won't make you rich, but locking in a 5% to 6% guaranteed return on a portion of your savings (enough to cover one or two years of expenses) can provide real peace of mind and a reliable income stream. Rates are expected to decline gradually as the Fed eases, so this window may not stay open forever.

7. Consider Part-Time Work to Supplement Retirement Income

Here's a statistic that surprised me: 92% of retirees don't have a side gig, but 60% wish they did.

Working 15 hours a week, whether that's consulting in your former field, freelancing, or driving for a rideshare company, can add $1,000 to $1,500 per month to your retirement income. That's $12,000 to $18,000 per year. Enough to meaningfully change your financial picture.

| Work Type | Hours/Week | Hourly Rate | Monthly Income | Annual Impact |

|---|---|---|---|---|

| Consulting (Former Field) | 10-15 | $75-100 | $1,200-2,400 | $14,400-28,800 |

| Rideshare Driving | 15 | $18-22 | $1,080-1,320 | $12,960-15,840 |

| Freelance Writing | 12 | $25-50 | $1,200-2,400 | $14,400-28,800 |

My man Dave is 66. He collects $1,800 per month in Social Security and $800 from a pension. He drives for a rideshare company about 15 hours a week, earning roughly $1,200 per month. After self-employment tax (about $183), he nets $1,017 in extra monthly income. He deducts mileage at 72.5 cents per mile, and since he's past his Full Retirement Age, there's no Social Security earnings test to worry about. He also likes getting out of the house and talking to people. Win-win.

For those considering this path, our guide on part-time retirement and healthcare bridge strategies covers how to maintain benefits while working reduced hours.

Tax-Smart Gig Income

Self-employed retirees can open a Solo 401(k) and defer up to $35,750 in employee contributions if they're age 60 to 63 (thanks to the SECURE 2.0 super catch-up provision), plus employer contributions of up to 25% of net self-employment income. That shelters gig income from taxes while building additional retirement savings. Pretty slick.

8. Max Out Your HSA Before Medicare

If you're still working and have a high-deductible health plan, your Health Savings Account is the single most tax-advantaged account available. Contributions are tax-deductible. Growth is tax-free. Withdrawals for qualified medical expenses are tax-free. No other account offers all three. It's the triple crown of tax advantages.

HSA: The Triple Tax Advantage

Tax-deductible contributions + tax-free growth + tax-free qualified withdrawals = the most powerful account in retirement planning. After 65, it works like a traditional IRA for non-medical expenses.

The 2026 limit is $4,400 for individuals and $8,750 for families, with a $1,000 catch-up for those 55 and older.

Karen is 58. She maxes her HSA at $5,400 per year (individual coverage plus her catch-up contribution) and invests it in index funds instead of spending it. Over seven years, she accumulates roughly $45,000 or more. Starting at 65, she uses it to cover Medicare premiums, dental work, and prescriptions completely tax-free. Every dollar she pulls from her HSA for medical expenses is a dollar she doesn't need to withdraw (and pay taxes on) from her IRA.

After age 65, an HSA works like a traditional IRA for non-medical withdrawals (you'll pay income tax but no penalty), and unlike a traditional IRA, it has no Required Minimum Distributions. It's a stealth retirement account hiding in plain sight.

9. Downsize Strategically for Immediate Income

Selling a larger home and moving to something smaller can unlock retirement income from multiple angles at once.

Before Downsizing

- Home Value $450,000

- Property Taxes $6,000/year

- Maintenance $3,000/year

- Annual Costs $9,000+

After Downsizing

- New Home $250,000

- Property Taxes $3,000/year

- Maintenance $2,000/year

- Investment Income $8,750/year

Jim and Pat sell their $450,000 home, buy a $250,000 condo, and invest the roughly $175,000 difference. At a 5% return, that generates $8,750 per year in investment income. They also save about $4,000 annually on property taxes, maintenance, and insurance. Combined, that's nearly $12,750 per year in improved cash flow. That's basically like adding a small pension.

The $250,000/$500,000 capital gains exclusion on a primary residence means most of the profit from selling is tax-free, making this one of the most tax-efficient ways to unlock equity.

Putting It All Together

The real power of these retirement income strategies isn't in any single move. It's in how they work together.

Delaying Social Security creates a window for low-cost Roth conversions. Roth conversions reduce future RMDs, which helps you avoid IRMAA surcharges. QCDs lower your taxable income further, potentially keeping you in a lower bracket. Withdrawal sequencing ties it all together by managing how much taxable income hits your return each year.

A couple who coordinates these moves across their 60s and 70s can end up with $10,000 to $25,000 more in annual after-tax retirement income compared to someone who takes the default path.

That's not theoretical. I've seen it play out with real people.

Keep in mind that traditional withdrawal rules like the 4% rule may not work in today's market environment, making these optimization strategies even more critical.

🎯 Your Next Three Steps

- Calculate your Social Security at different claiming ages using SSA.gov's calculator. Run the numbers for 62, 67, and 70. Seeing your own dollar amounts makes the decision real in a way that reading an article never can.

- Map your retirement income valley. What year will you retire? What year will RMDs begin? That gap is your planning window for Roth conversions, 0% capital gains harvesting, and benefit timing.

- Talk to a fee-only financial planner about strategy interplay. A one-time planning session (typically $1,000 to $3,000) focused on tax-efficient withdrawal sequencing and Social Security timing can easily pay for itself many times over in the first year alone.

Your retirement income isn't set in stone the day you stop working. With the right moves at the right time, it's something you can actively grow.

Thanks for reading if you've made it this far. Peace!